Rumored Buzz on Mortgage Investment Corporation

Rumored Buzz on Mortgage Investment Corporation

Blog Article

The 4-Minute Rule for Mortgage Investment Corporation

Table of ContentsHow Mortgage Investment Corporation can Save You Time, Stress, and Money.The Single Strategy To Use For Mortgage Investment CorporationThe Best Guide To Mortgage Investment CorporationThe Mortgage Investment Corporation DiariesOur Mortgage Investment Corporation Statements

Does the MICs credit history board review each home mortgage? In most circumstances, mortgage brokers manage MICs. The broker needs to not act as a member of the credit history board, as this puts him/her in a direct dispute of interest provided that brokers generally make a compensation for positioning the home mortgages.Is the MIC levered? The monetary organization will certainly accept particular mortgages possessed by the MIC as safety and security for a line of credit report.

It is vital that an accountant conversant with MICs prepare these declarations. Thank you Mr. Shewan & Mr.

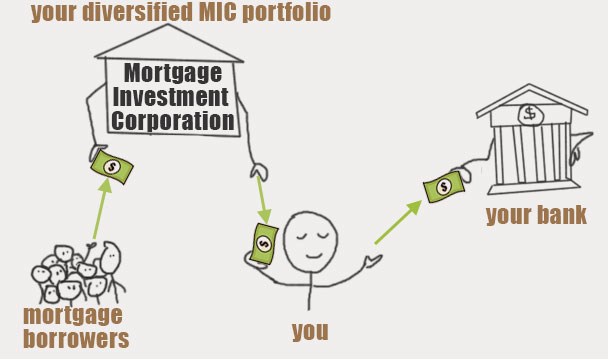

Last updated: Nov - Mortgage Investment Corporation. 14, 2018 Few investments couple of financial investments advantageous as a Mortgage Investment Home mortgage (Company), when it comes to returns and tax benefits. Since of their company structure, MICs do not pay revenue tax and are legitimately mandated to distribute all of their incomes to investors.

This does not indicate there are not risks, however, usually speaking, whatever the broader securities market is doing, the Canadian genuine estate market, particularly significant municipal areas like Toronto, Vancouver, and Montreal performs well. A MIC is a firm formed under the policies establish out in the Income Tax Act, Area 130.1.

The MIC earns earnings from those home loans on passion charges and general charges. The actual appeal of a Home loan Financial Investment Firm is the yield it offers financiers contrasted to various other fixed income investments. You will certainly have no problem finding a GIC that pays 2% for an one-year term, as government bonds are equally as reduced.

Some Known Questions About Mortgage Investment Corporation.

A MIC needs to be a Canadian corporation and it have to invest its funds in mortgages. That claimed, there are times when the MIC ends up possessing the mortgaged residential property due to foreclosure, sale arrangement, etc.

A MIC will make interest earnings from mortgages and any kind of money the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to investors, the MIC does not pay any revenue tax. As opposed to the MIC paying tax on the rate of interest it earns, shareholders are accountable for any type of tax obligation.

The smart Trick of Mortgage Investment Corporation That Nobody is Talking About

And Deferred Plans do not pay any type of tax on the rate of interest they are estimated to get - Mortgage Investment Corporation. That claimed, those who hold TFSAs and annuitants of RRSPs or RRIFs may be hit with specific fine taxes if the financial investment in the MIC is thought about to be a "prohibited visit homepage financial investment" according to copyright's tax obligation code

They will ensure you have located a Home loan Financial investment Corporation with "certified investment" condition. If the MIC certifies, it could be extremely beneficial come tax obligation time given that the MIC does not pay tax on the passion income and neither does the Deferred Plan. A lot more generally, if the MIC fails to satisfy the needs set out by the Earnings Tax Act, the MICs websites revenue will certainly be taxed before it gets dispersed to investors, decreasing returns considerably.

It shows up both the actual estate and supply markets in copyright are at all time highs Meanwhile yields on bonds and GICs are still near document lows. Also cash money is losing its appeal since power and food rates have actually pressed the inflation rate to a multi-year high.

Some Known Details About Mortgage Investment Corporation

Many hard working Canadians who wish to buy a house can not obtain home mortgages from traditional financial institutions due to click to read more the fact that probably they're self used, or do not have an established credit rating yet. Or possibly they want a short-term loan to create a large residential property or make some renovations. Financial institutions have a tendency to neglect these potential debtors since self used Canadians don't have stable revenues.

Report this page